What's your number?

a (sometimes triggering) tool for curbing loss aversion while paying off debt

Let’s recap.

I’ve explained how my debt repayment journey started, how I realized I was spinning my wheels and why and the imperfect guru who charted my path forward.

The only way that I could begin to execute that plan was to build a budget.

So then I paused to try to rebrand budgeting as an idea (despite its terrible name) and explain why tracking expenses (despite out tedious it sounds) became my method for budgeting consciously.

Today I’m going to talk about another element of the debt repayment budget I built.

It’s a number. I keep track of in my budget spreadsheet to this day.

It made it psychologically easier for me to make debt payments.

The thing is…

I think it has an even more triggering name than “budget.”

It can bring up conscious and subconscious feelings around adequacy and security.

It brings you face-to-face with a kind of basic truth of your overall financial situation.

It is something to take seriously, but it is not everything.

So, strap in!

My number

I deleted my Instagram a while back, but while I was paying off debt I distinctly remember a post I put up with two photos side-by-side.

The first:

The second:

The caption was something like: “These days I oscillate between these two extremes.”

The thing is, the second meme was right about me.

Financially, I was actually worth less than $0.

Because I did the math.

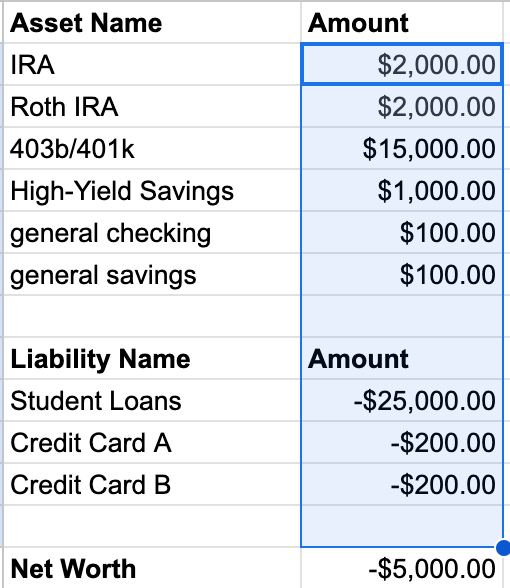

I calculated my Net Worth.

What Net Worth Is

Your Net Worth is a math equation:

Assets - Liabilities = Net Worth

Assets are things you have: retirement accounts, checking accounts, savings accounts, the value of a car, equity in a house, etc.

Liabilities are things you owe: credit card debt, student loan debt, car loans, a mortgage, crushing American-brand medical debt, etc.

In my budget spreadsheet, I typed in the totals of all of my assets and liabilities (the liabilities are negative numbers, of course).

Then I highlighted the relevant columns and pressed the little sigma symbol on the top row of my spreadsheet to calculate the sum. That number was my net worth.

When I did this, the total number was negative, as it is in the example above.

I had money in my checking, savings and retirement accounts, but I had more money that I owed in student loans.

What Net Worth Isn’t

This should go without saying but:

Your Net Worth is not a reflection of your worth as a human being.

It is a broad view of your financial health in this current moment.

But I think one reason people don’t like to talk about money is because they subconsciously confuse their self-worth with their net worth anyway.

I don’t know who needs to hear this but having a lot of money, not having a lot of money — neither determines how “good” or “worthy” of a person you are.

I think the fact that I was raised by a mom who was a literal African orphan as a child helped me understand this in my bones. My mother did not raise me to necessarily equate wealth with honor or evil; poverty with poor or inherently noble character. She’d met angels and a-holes of all economic stripes, in rich times and poor times.

She ended up with a comfortable economic existence in America and does not feel guilty for that. She feels very grateful for the good fortune and also created conditions long ago to influence her fate.

Your fortunes can change dramatically. You are not a better or worse person because your fortunes have changed.

I have just as much respect and affection for the version of me with a negative net worth in 2018 as I do for the me today with a positive net worth. The me in early 2018 had less awareness of her situation. I won’t internally berate her for that. She made changes that I’m benefitting from today because she took action once she realized the predicament she was in.

In the society we live in today, there is more wiggle room to navigate the inevitable ups and downs of life with more financial resources. I would like those additional resources, but I don’t expect those additional resources to define what I am worth as a person.

This is not everyone’s mindset, but it’s been a non-financial asset1 for me.

An antidote to loss aversion

No matter the feelings calculating your Net Worth brings up, it is a powerful tool for anyone who’s trying to pay down their debt.

Something that feels psychologically difficult about paying back huge amounts of debt is that you feel like you’re giving up your hard-earned money.

Your money is leaving your bank account to fill up a deep, deep pit (that only grows a little deeper every day thanks to interest).

We humans hate to lose what we have:

“Loss aversion refers to the relative strength of two motives: we are driven more strongly to avoid losses than to achieve gains.”

- Daniel Kahneman, Thinking Fast and Slow

But paying attention to your Net Worth while you’re paying off debt is a way of seeing your “loss” as a big picture gain.

Because with every debt payment you make, the negative numbers in the liabilities section of your budget inch toward zero.

So while it could feel as though I was losing extra money by throwing it at my debt, my Net Worth tab could show me a different, broader story.

Every debt payment I made was growing my Net Worth.

I used several other methods for tracking my progress that accelerated the whole process. Paying off my debt in two years wasn’t actually the plan — it’s just that the systems I had in place — updating my Net Worth, a payday routine, an anonymous community I found, and luck — sped up the whole endeavor.

More on those accelerants in subsequent posts.

— Bethel

P.S. If any of this is hitting home for you, I’d love to hear from you in the comments or dms. I especially want to hear about anyone else who has grappled with self-worth/net worth feelings.

ETC.

“[hearty laughter] Children - it's not worth it.” - IronChefdad

(thanks to my nephew J. for sharing this with me!)“Nothing is ever as good or as bad as it seems.” - Scott Galloway (man, do I love when I see other people admit that we have what we have/don’t have is largely a product of luck).

A systems therapist with a word.

My first memory of the words “asset” and “liability” were in an entirely different context — in a pivotal scene in the classic movie The Princess Bride. The assets discussed were the individual skills of the people trying to rescue the princess - one guy’s brains, one guy’s brawn, one guy’s swordsmanship, and a reaper robe. The liabilities were the hoards of men guarding the castle.

I like this way of thinking about assets. A degree, an alumni network, friends, those are all assets in one’s toolbox — but not in one’s spreadsheet — that can translate into desirable financial and non-financial outcomes. A supportive family can be an asset when you’re processing the death of a parent or navigating a health scare. Good friends can help us through break ups. We can consciously make investments in these non-financial asset categories — and stay awake when the pursuit of wealth diverts too much energy from them — because they are what help us live a good life.

Similarly, there can be non-numerical liabilities in your life — a job that drains you to the point of developing an autoimmune disease. A relationship that drives you to self-medicate with alcohol.

This is why “your number” is something, but isn’t everything. Vicki Robin, who I’ll talk about in future posts, really illustrates this point well in her book “Your Money or Your Life.”

I like your take on the discussion of the “B” word. In my line of work it’s the “R” word. I’ve also been where you have and had a plan to get where I am now, using those intangible assets that don’t show up on a net worth statement.